2021 in review. Predictions for the year ahead.

2021 will be remembered as the year of high inflation and low supply. Philipp Omenitsch provides an economic outlook on how he sees the coming year shaping up.

The rally in the financial markets in the last year was mostly caused by extremely low-interest rates and quantitative easing by central banks. In the coming year, 2022, fluctuations in the financial markets will mostly be dependent on inflation and, in particular, changes in interest rates. Before I move on to a discussion of the year ahead, let’s take some time to review the year that has just ended: 2021.

Supply chains and bottlenecks

When we look back at 2021 some problems have been way more persistent than we thought. While Covid-19 came down like the sword of Damocles upon us, crushing stock markets and any positive outlook, we quickly saw a rebound after a couple of months. This unprecedented variation in demand had a huge impact on global supply chains. Pre-covid our world and especially our supply chains were not optimal. However, for the most part, they were predictable. If the economy took a plunge, car dealers or car manufacturers, for example, could feel that change weeks (if not months) in advance via fewer orders. Thus, they could plan their production accordingly.

Covid-19 was completely different. On the one hand, some industries saw declines in their orders of 20%, 50%, or more within days or weeks. On the other hand, the uptick in sales was just as sudden and surprising when the economy began to restart, 2020 and 2021.

After the first big shock of 2020 — with help of fiscal and monetary stimulus packages and the central banks offering record-low interest rates—people began to catch up on the expenditures they had put off. This included purchases like the TV they didn't buy, but still needed or wanted, because shops were closed. There was also an unprecedented demand for home office equipment. Let’s not forget the car they held off on buying until the economic climate turned more positive. With record-low interest rates, it suddenly seemed like the perfect time to make that large purchase. There are many more similar examples. This led to orders overshooting what manufacturers were able to produce, especially with little lead time.

With long supply chains, it takes time for this sudden increase in demand from the consumer to reach a manufacturer on the other side of the world.

Because it is difficult to scale up physical production facilities (like we saw with face masks at the beginning of the pandemic), producers can’t adapt quickly to unpredicted increases in demand. This is especially evident in industries where scaling up takes years or lead times are long (such as computer chip manufacturing). Furthermore, it simply might not make sense for many producers to increase production. Firstly, they can charge more for their product now that demand is high and supply is limited, and secondly, they are familiar with what steady demand looks like from pre-Covid times, so they might not want to increase their production levels today and have a surplus and idle production capabilities two or three years from now.

I like to think of this effect like the pendulum in a clock. It usually swings left and right with very little variance; however, if you push the pendulum further to one side, it will swing back harder to the other side. This is similar to how Howard Marks, in his great book Mastering the Market Cycle, (and Ray Dalio has also touted this) describes cycle swings, but it’s a little different in this case.

Russian Chicken Farms

Since this is all very abstract and global supply chains are a very complex system, I would like to share with you an example I’m aware of from a Russian chicken farmer. It perfectly illustrates how difficult it is for markets to regulate production capabilities, even for “simple” supply chains. The local market price for chicken meat in Russia is free-floating; thus, it is also subject to variations in its price. The market knows roughly how much meat is needed at any given time. For example, it is understood that more chicken will be needed before the holidays. You would imagine that the price is therefore not subject to much change. Since it takes roughly 35 days to raise a chickling to a proper size, a chicken farmer needs to estimate how much demand there will be for chicken 35 days from now, so he or she can decide how much chicken to raise in each batch. And now for the interesting part: there are, of course, multiple large chicken producers, and every producer wants to maximize their profits. So, ideally, they must all grow as much chicken as they can sell at a profit, ideally when the price is high, and less so when the price is low. But what is the best way to estimate this?

It turns out, one can not accurately predict the market price without knowing exactly how much your competition will produce. If you think about it, the best indicator for the price in 35 days is the price today. Game theory tells us it would be best if all market participants shared information. However, this would probably manifest as a cartel. So what happens is, when the price is high, everybody grows lots of chicken, thus crashing the price in 35 days and causing price swings of about 30%! When I first heard about this, I couldn’t believe it. It’s crazy but it’s true.

In my opinion, this is EXACTLY what's going on in the general economy today. Production with large lead times, monopolies or oligopolies, and highly protected markets are the most affected by unforeseen changes in demand. And to some extent, we have witnessed this with chip manufacturers, but also with airplane producers, ship producers, and other industries that had their logistics disrupted by Covid-19.

My prediction is that over time, we will get back to the same level of predictability of supply that we experienced pre-Covid, even for inelastic industries with long lead times. Most likely, chip manufacturers will be affected for a longer time still, but this is also due to ASML having a de facto monopoly and producing almost all the EUV lithography machines needed to scale up modern IC production.

All of this, demand overshooting supply, and low-interest rates, have led to a rate of inflation not seen in the US since 1982.

It will be interesting to see if, how hard, and when the pendulum swings back.

Interest rates

The above explanation of inflation nicely aligns with the FEDs (American central bank) stance on “transitory inflation” and their interest rate policy. Over a long enough timeframe, the pendulum should swing back and cancel out any price increases. However, the pendulum is also swinging slower than many would have expected because the pandemic is still ongoing and lasting much longer than expected. Since inflation has now been high for an extended period of time, it is starting to have a ripple effect. People who had been waiting for prices to normalize may now think they have been waiting too long. Believing that their money is devaluing, they feel compelled to spend it. Better buy that house now since inflation is high and interest is low. There might not come a better time!

Thus, the FED is forced to make a tough decision about increasing interest rates. In my opinion, it is not clear that inflation will immediately react to this because the fundamentals of supply will not change. In fact, on the contrary, it might even stifle investments. However, it will have an effect on assets being purchased on credit, because credit gets more expensive with higher interest rates. Personally, I am expecting the FED to hike rates quite aggressively, more so than many people think and they themselves predict, but also lower them again quickly when the pendulum swings back.

As for Europe, I think they are in a better position because people are less aggressively taking advantage of the low-interest rates. Consequently, there is less inflation pressure from asset purchases on credit and leverage.

Predictions

Stocks

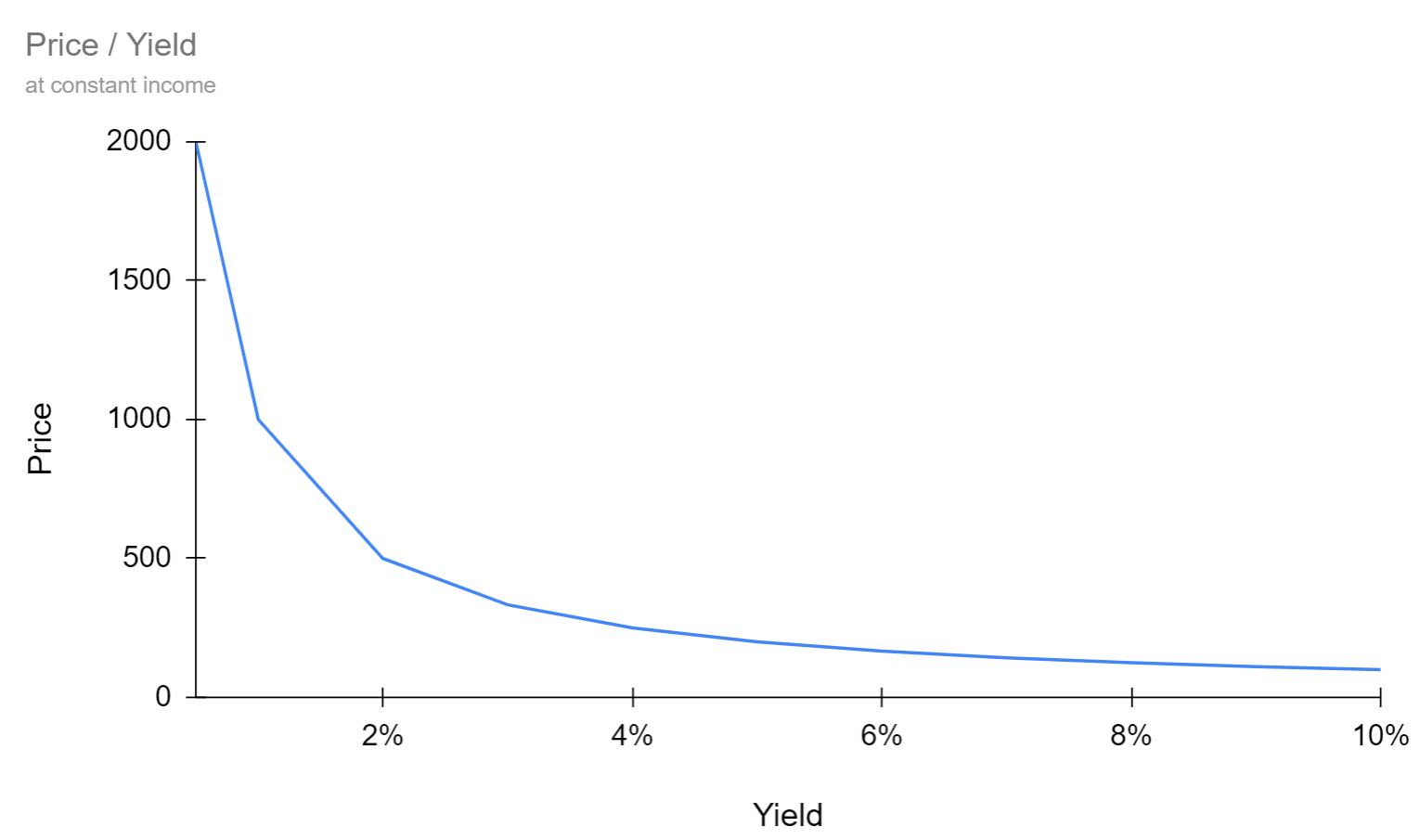

For stocks, I want to outline one observation that in my eyes is often overlooked. A fundamental effect that tricks our brains.

In the chart above, I’ve tried to demonstrate why even a small increase in interest rates can have a dramatic impact on asset prices at the current level. I’ve calculated the price of a fictional stock with constant earnings for different yields, because a stock, in my opinion (Warren Buffet agrees), can be seen as a yield earning asset with a risk premium compared to bonds. A small interest rate increase at very low rates has a much higher impact than at higher yields. This is what math tells us.

Stocks will behave differently depending on the industry. Technology stocks, in my view, are especially inflated because of low-interest rates, so I definitely see them losing ground in the year ahead. In contrast, value stocks profiting from the high prices and low supply will benefit. It is easier to justify high future revenues for high margin businesses with little capital expense than for capital intensive businesses. High Tech company valuations often come from investors valuing them with Discounted Future Cashflow and this method strongly depends on the discount (interest) rate.

Real estate

For real estate purchases, interest rates are a driving factor, but other components include investor appetite for real estate, population growth, and supply. The last factor, supply, is particularly cyclical and highly dependent on the region in question.

In general, though, driven by the first and most important factor, debt, I think real estate will suffer as a result of increasing interest rates. It is unlikely that we will see a huge, sudden drop, but I can see prices stabilizing or dropping slightly when interest rates rise.

Crypto

Crypto is very interesting to look at and the most difficult asset to predict. This is because of its huge value fluctuations in the past and because of a lack of fundamentals. It is often touted as a hedge against inflation, and I largely agree with this for the blue-chips (Bitcoin, Ethereum, etc.). In any case, a higher interest rate will certainly hurt cryptocurrencies because they don't provide any yield and they are competing with higher-yielding assets, like bonds and stocks even more so with rising interest rates. Many DeFi products do promise yield, and it will be very interesting to see how they behave in the event of a larger downswing. I see many (not all, though) of them as very risky, but some even see them as highly complex financial instruments.

Startup valuations

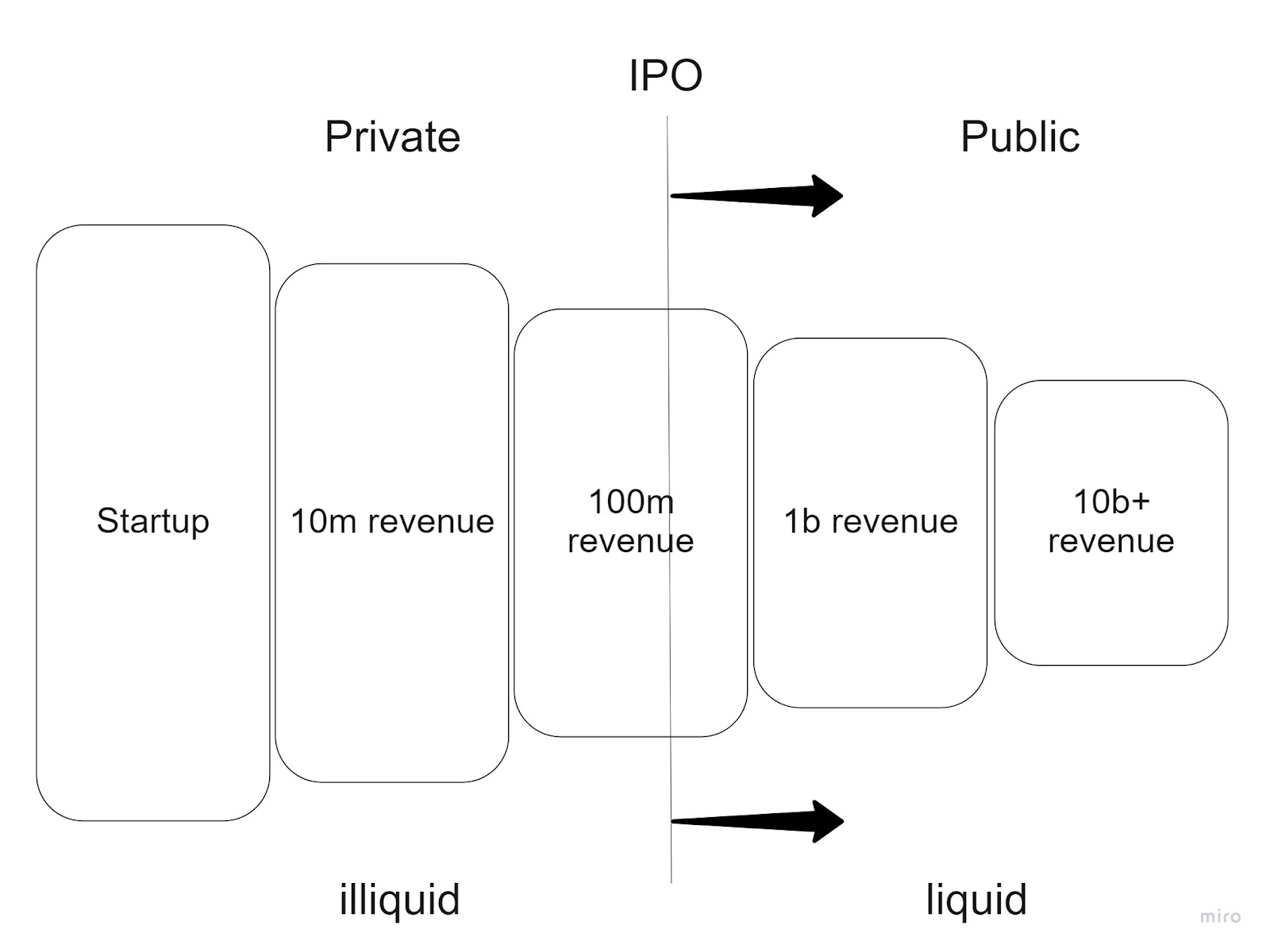

Over the last decade, we have witnessed a focused pursuit of yields. Pension funds and investors— because of the low-interest-rate environment—have been driven to pursue riskier assets, especially when compared to purchasing bonds that yield a return that is satisfactory to their needs. To maintain their previous levels of yield, investors have now piled into equities and, increasingly, into private equity and earlier stages of company funding. From creation to private fundraising, to IPO. Investors are now trying to capture higher yields by entering deals earlier (as opposed to IPO or post-IPO). Thus, we’re witnessing a dramatic increase in venture funding (investment before profits are made) and startups staying private for longer because they can (financing exists that enables it). Another point is the rise of SPACs, which allow companies to go public earlier through some clever tricks (often even pre-revenue).

I’ve already covered how inflation is most likely leading us to rising interest rates. Now, I want to quickly discuss what impacts this will have on startup funding. Current valuations are historically high and have been accelerating at an astonishing rate.

One reason for this dramatic rise is that returns have been higher in private markets for some time. Now, investors are trying to get those returns by increasingly entering private markets. This has allowed companies to stay private for longer and go public later.

Why am I bringing this up? As can be seen in the chart above, this has caused investments to become more and more illiquid, even though there is now a huge shadow market where shares in private companies can be traded (i.e., EquityZen) and a range of investment platforms to invest in companies at earlier stages easier (i.e., AngelList, Republic, etc.).

If interest rates rise, I expect at least some of those high startup valuations to decrease. Or rather, I predict fewer funding rounds for startups that are bleeding money, which could lead to more defaults. However, because those assets are inherently illiquid, those effects will be magnified.

Thus, I recommend being very careful when dealing with startups with high valuations, when interest rates rise, those might be deflated one way or the other.

Closing Thoughts

Covid-19 has changed the world and its effects will long be felt throughout the world. I hope that supply chains will become more robust as one outcome of this. It will be interesting to observe if getting out of the lowest interest rate environment in decades without hurting economies will be possible. I am optimistic that we will adapt to the environment, I am positioning for rising interest rates, they will come sooner or later.

Photo by Rinson Chory on Unsplash

Photo by Jan Baborák on Unsplash